Digital Transformation in Corporate Banking: 2026 Guide

Quick Summary: Digital transformation in corporate banking refers to the integration of advanced technologies—AI, cloud computing, blockchain, and data analytics—into banking operations to streamline processes, enhance client experiences, and maintain competitiveness. This shift goes beyond digitization; it fundamentally reimagines how corporate banks deliver services, manage risk, and collaborate with fintech partners in an increasingly digital financial ecosystem.

The banking sector is experiencing a fundamental shift. Corporate banking, traditionally characterized by relationship-driven services and complex manual processes, now stands at a technological crossroads. The pressure isn't just about keeping pace—it's about survival.

Digital technologies have moved from optional enhancements to core infrastructure. Banks that embraced transformation early are pulling ahead, while those hesitating face existential threats from nimble fintech startups and tech giants entering financial services.

But here's the thing: digital transformation in corporate banking isn't simply about installing new software or launching a mobile app. It's a comprehensive reimagining of how banks operate, deliver value, and interact with corporate clients.

What Digital Transformation Really Means for Corporate Banking

Digital transformation integrates technology across every banking function—from front-office client services to back-office operations. The goal extends beyond efficiency gains to fundamentally changing how banks create value.

According to MIT Sloan Management Review and Deloitte's 2015 global study, only 15% of respondents from companies at the early stages of digital maturity have a clear and coherent digital strategy. Among digitally maturing organizations, more than 80% do.

The difference? Strategy drives technology adoption, not the other way around. Banks that succeed in transformation start with business objectives—improving client experience, reducing operational costs, managing risk better—then select technologies that serve those goals.

Beyond Digitization: The Strategic Shift

Digitization converts analog processes to digital formats. Transformation redesigns those processes entirely. A corporate bank that scans loan applications is digitizing. One that uses AI to assess creditworthiness in real-time, automatically structure deals, and provide instant approvals is transforming.

The distinction matters. Digitization improves existing workflows incrementally. Transformation creates entirely new capabilities and business models.

Modernize Banking Systems With OSKI

OSKI builds custom software and AI integrations for companies that need reliable tools around existing business systems. Their work covers backend development, frontend interfaces, API integrations, cloud setup, DevOps, and long-term support.

For corporate banking teams, this can support internal portals, reporting tools, workflow automation, data integrations, or AI features for document-heavy and process-heavy operations.

Need Software Built Around Banking Workflows?

OSKI can help with:

developing custom business software

integrating internal and external systems

adding AI and automation features

supporting secure cloud deployment

👉 Contact OSKI to discuss your project.

Digital Transformation in Corporate Banking

Modernize banking operations with AI, automation, and connected financial systems.

Key Technologies Driving Transformation

Several core technologies power the transformation wave sweeping through corporate banking. Each brings distinct capabilities, and their real power emerges when combined strategically.

Artificial Intelligence and Machine Learning

AI transforms everything from credit risk assessment to fraud detection. Machine learning models analyze patterns in vast datasets faster and more accurately than human analysts.

Corporate banks deploy AI for:

Automated credit scoring and loan underwriting

Real-time fraud detection and prevention

Predictive analytics for cash flow management

Chatbots and virtual assistants for client service

Regulatory compliance monitoring

The technology isn't theoretical. Banks report measurable improvements in processing speed, accuracy, and cost reduction once AI systems mature.

Cloud Computing Infrastructure

Cloud infrastructure provides the scalability and flexibility legacy on-premise systems can't match. Corporate banks historically ran everything on proprietary hardware—expensive, inflexible, and difficult to update.

Cloud adoption allows banks to scale compute resources on demand, deploy new services faster, and reduce capital expenditure on hardware. Security concerns that initially slowed adoption have largely been addressed through improved encryption, compliance certifications, and hybrid cloud models.

Blockchain and Distributed Ledger Technology

Blockchain is moving beyond cryptocurrency hype into practical banking applications. The technology excels at creating transparent, immutable records of transactions—valuable for trade finance, syndicated lending, and settlement processes.

According to Federal Reserve Governor Lisa D. Cook's May 8, 2026 speech on tokenization, tokenized assets in the U.S. more than doubled their market capitalization in the last year to around $25 billion.

These aren't pilot programs—they're production systems handling real institutional volume.

Advanced Data Analytics

Corporate banks sit on mountains of data. Transaction histories, client interactions, market data, operational metrics—the volume is staggering. Advanced analytics platforms turn that raw data into actionable intelligence.

Banks use analytics to identify cross-selling opportunities, optimize pricing, predict client churn, and personalize services. The competitive advantage flows to institutions that can extract insights faster and act on them more effectively.

Strategic Imperatives for Corporate Banks

Technology alone won't guarantee successful transformation. Banks need clear strategies that align technology investments with business outcomes. Several strategic imperatives emerge consistently among successful transformations.

Client Experience as the North Star

Corporate clients now expect consumer-grade digital experiences. Clunky interfaces, slow response times, and multi-day processes won't cut it when fintech competitors offer instant solutions.

Banks must design services around client needs, not internal processes. That means intuitive interfaces, transparent pricing, real-time information, and seamless omnichannel experiences.

According to Deloitte research, 61% of customers are willing to switch to a digital bank. The message is clear: improve the experience or lose the client.

Data as a Strategic Asset

Banks that treat data as a byproduct of transactions leave value on the table. Leading institutions recognize data as perhaps their most valuable asset—one that generates insights, drives decisions, and creates competitive advantages.

This requires investing in data infrastructure, governance frameworks, and analytics capabilities. It also means breaking down data silos that prevent comprehensive views of client relationships and operational performance.

Agile Operating Models

Traditional banking operates on long planning cycles and waterfall project management. Digital demands speed and adaptability. Banks need agile operating models that can pivot quickly as markets, technologies, and client needs evolve.

This isn't just about development methodology—it's a cultural shift. Cross-functional teams, iterative delivery, experimentation, and tolerance for failure become organizational norms.

Ecosystem Thinking and Collaboration

No bank can build everything in-house. The winning strategy involves selective partnerships with fintech companies, technology providers, and even competitors in certain contexts.

Platform approaches that integrate third-party services through APIs create richer client experiences than closed systems. Banks become orchestrators of financial ecosystems rather than vertically integrated fortresses.

The Fintech Partnership Model

The relationship between banks and fintech companies has evolved dramatically. Early narratives positioned fintechs as disruptive threats that would render traditional banks obsolete. Reality proved more nuanced.

Fintechs bring innovation, agility, and customer-centric design. But they often lack regulatory expertise, capital reserves, and the trust that comes with established brands. Banks possess those strengths but struggle with legacy systems and slow innovation cycles.

The result? A collaborative model emerges where banks and fintechs partner rather than compete. Banks provide infrastructure, regulatory compliance, and balance sheet strength. Fintechs contribute technology platforms, user experience design, and speed to market.

This symbiotic relationship accelerates innovation for both parties. Banks gain access to cutting-edge capabilities without building from scratch. Fintechs access distribution networks and regulatory frameworks that would take years to develop independently.

Real-World Partnership Examples

Treasury management platforms built by fintechs integrate with bank systems to provide corporate clients with unified cash visibility across multiple banking relationships. Lending platforms use alternative data and machine learning to expand credit access while banks provide capital and regulatory oversight.

Payment networks connect bank infrastructure with merchant services, e-commerce platforms, and mobile wallets. Trade finance platforms digitize documentary processes while banks maintain correspondent relationships and compliance functions.

Implementation Challenges and Solutions

Digital transformation sounds compelling in strategy documents. Execution is where most initiatives stumble. Corporate banks face distinct challenges that require thoughtful solutions.

Legacy System Integration

Core banking systems at many institutions date back decades. They're stable and reliable but weren't designed for the digital age. Replacing them entirely poses enormous risk and cost.

The solution often involves gradual modernization—wrapping legacy systems in modern APIs, migrating specific functions to cloud platforms, and building new capabilities alongside old systems rather than ripping and replacing.

Regulatory Compliance and Security

Banks operate in heavily regulated environments. Any technology change must satisfy regulators regarding data protection, financial stability, and consumer protection. Security concerns multiply as banks open APIs and connect to external platforms.

According to TierPoint research, 91% of Americans decide which bank to use based on fraud protection and other security features, placing it on equal footing with quality customer service and digital banking access.

Solutions require security-by-design approaches, robust identity management, continuous monitoring, and close collaboration with regulators to demonstrate compliance while innovating.

Talent and Culture

Technology transformation ultimately depends on people. Banks need talent with skills in data science, cloud architecture, agile development, and user experience design—capabilities that don't traditionally exist in banking organizations.

Cultural resistance poses an equally significant challenge. Employees comfortable with established processes resist change. Risk management functions see new technologies as threats rather than opportunities.

Addressing these requires comprehensive change management: clear communication from leadership, training programs, incentive alignment, and celebrating early wins to build momentum.

Measuring Transformation Success

How do banks know if digital transformation is working? The metrics that matter extend beyond technology adoption to business outcomes.

Leading banks establish transformation offices that track these metrics, identify bottlenecks, and adjust strategies based on results rather than assumptions.

The Role of Payments in Digital Transformation

Payment systems sit at the heart of banking transformation. Every corporate banking relationship involves moving money, and how efficiently that happens fundamentally shapes client satisfaction.

According to the Bank for International Settlements (BIS Annual Economic Report, June 2020), retail payments make up nearly 90% of the total volume of payments (by number of transactions), yet less than 1% of the total value. Wholesale payment systems—where corporate banking operates—handle enormous value with relatively few transactions.

This creates different optimization opportunities. Retail payments focus on convenience and speed. Wholesale payments prioritize security, certainty, and integration with treasury management systems.

Digital transformation enables real-time payment capabilities, transparent tracking, automated reconciliation, and seamless cross-border transactions—capabilities that directly impact corporate client operations.

Global Payment Platforms

The scale of digital payment platforms globally is staggering. According to Federal Reserve data cited in a 2020 speech by Governor Lael Brainard, Alipay and WeChat Pay handled more than $37 trillion in mobile payments.

Even non-bank entities like Walmart and Starbucks hold significant payment float—SOFTEN to: 'Major retailers like Walmart and Starbucks hold significant payment float through gift card and stored-value card programs.'

These examples illustrate how payment capabilities transcend traditional banking boundaries. Corporate banks must compete in this expanded ecosystem.

Emerging Trends Shaping the Future

Several trends are currently reshaping corporate banking's digital landscape. Banks that understand and adapt to these trends position themselves for sustained relevance.

Tokenization and Digital Assets

Tokenization—representing real-world assets as digital tokens on distributed ledgers—is gaining institutional traction. The Federal Reserve noted that tokenized assets in the U.S. more than doubled to around $25 billion, with repo platforms processing $8 trillion daily.

This represents more than technological curiosity. Tokenization promises faster settlement, fractional ownership, 24/7 markets, and programmable assets with embedded smart contracts that automate complex processes.

Embedded Finance

Financial services are increasingly embedded in non-financial platforms. Corporate clients expect to access banking services within their ERP systems, procurement platforms, and operational tools—not by logging into separate banking portals.

This requires banks to offer modular services through APIs that integrate seamlessly into client workflows. The bank becomes invisible infrastructure rather than a destination.

Sustainable Finance Integration

Environmental, social, and governance considerations are moving from peripheral concerns to core banking criteria. Corporate clients demand sustainability-linked financing, carbon accounting, and ESG reporting integrated into banking platforms.

Digital transformation enables this integration by connecting financial data with environmental metrics, automating ESG disclosure, and providing transparency into supply chain impacts.

Best Practices for Transformation Success

Banks that successfully navigate digital transformation share common practices. These aren't theoretical principles—they're battle-tested approaches from institutions that have delivered measurable results.

Start with Strategy, Not Technology

The temptation to chase shiny new technologies is strong. Resist it. Begin with clear business objectives: What client problems need solving? What operational inefficiencies demand attention? What competitive threats require response?

Only after defining strategic goals should technology selection begin. This ensures investments align with business needs rather than becoming expensive experiments.

Adopt Platform Thinking

Banks that build isolated point solutions create technical debt and integration nightmares. Platform approaches—modular, API-connected architectures—provide flexibility to add capabilities, swap components, and evolve as needs change.

Platform thinking extends beyond technology to business models. Create ecosystems where partners contribute specialized capabilities while the bank orchestrates the overall experience.

Prioritize Client Co-Creation

Banks that design services in isolation from clients often miss the mark. Involve corporate clients throughout the development process. Understand their workflows, pain points, and priorities. Test prototypes early and iterate based on feedback.

This client-centric approach ensures solutions address real needs rather than perceived problems.

Balance Speed with Risk Management

Banking requires prudent risk management. But risk aversion that prevents all experimentation guarantees obsolescence. The solution lies in structured innovation frameworks: controlled experiments, small initial deployments, clear success criteria, and kill switches if problems emerge.

This allows innovation while maintaining the safety and soundness regulators and clients expect.

Invest in Talent Development

Technology platforms can be purchased. The organizational capability to use them effectively requires developing people. Invest heavily in training, create career paths for digital roles, and bring in external talent to seed new capabilities.

Consider transformation a people challenge with a technology component rather than the reverse.

Conclusion: The Path Forward

Digital transformation in corporate banking isn't optional—it's existential. The banks that embrace comprehensive transformation will strengthen client relationships, improve operational efficiency, and position themselves for sustainable success. Those that delay or approach transformation incrementally risk competitive irrelevance.

The path forward requires clear strategy, sustained investment, cultural change, and patient persistence. Technology provides the tools, but transformation succeeds or fails based on how organizations deploy those tools in service of client needs.

The good news? Corporate banks possess inherent advantages—client trust, regulatory expertise, financial strength—that position them well if they act decisively. The question isn't whether transformation is necessary. It's whether institutions will move fast enough to lead the change rather than react to it.

Now is the moment to assess your institution's digital maturity, identify strategic priorities, and commit to the sustained effort transformation requires. The competitive landscape will look dramatically different in five years. The actions taken today determine where banks land in that future landscape.

Frequently Asked Questions

What's the difference between digital transformation and digitization in banking?

Digitization converts analog processes to digital formats—like scanning documents or moving spreadsheets to cloud storage. Digital transformation fundamentally redesigns processes using digital capabilities, creating new business models and ways of delivering value. Digitization improves efficiency incrementally; transformation changes what's possible entirely.

How long does digital transformation take in corporate banking?

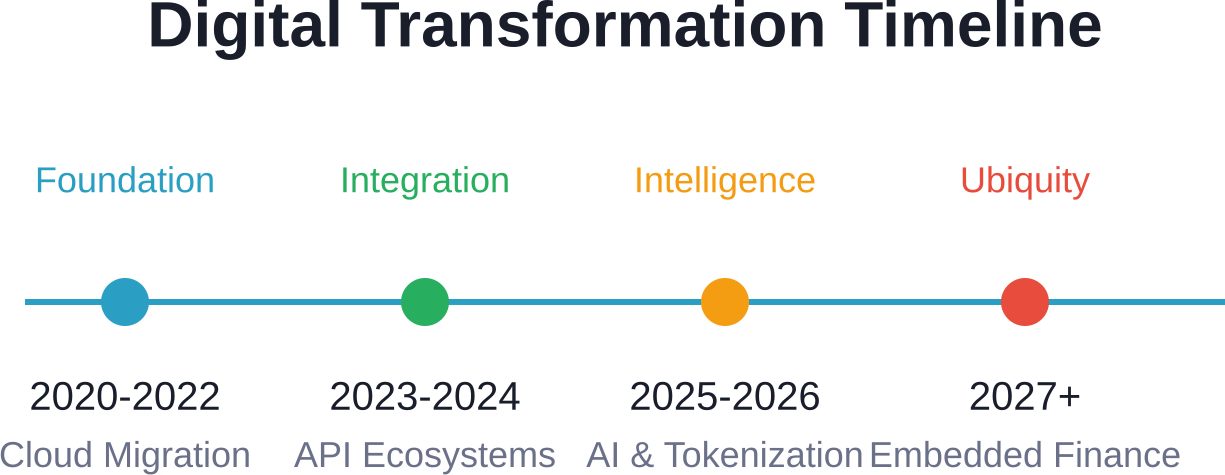

There's no single timeline because transformation is continuous rather than a one-time project. Foundation-building—cloud migration, API infrastructure, core system modernization—typically takes 2–4 years. But transformation itself is an ongoing journey of iteration, learning, and adaptation as technologies and client needs evolve. Banks that think transformation has an endpoint misunderstand its nature.

What are the biggest obstacles to digital transformation in banking?

Legacy technology systems represent the most visible challenge, but organizational culture and talent gaps often prove more difficult. Banks built on hierarchical, risk-averse cultures struggle with the experimentation and speed digital demands. Regulatory complexity adds another layer, requiring careful navigation to innovate while maintaining compliance. Finally, the sheer scale and complexity of banking operations makes coordinated change exceptionally difficult.

How do corporate banks balance innovation with security requirements?

Leading banks adopt security-by-design principles where protection mechanisms are built into systems from inception rather than added afterward. They use zero-trust architectures, continuous monitoring, robust identity management, and extensive testing. Regulatory sandboxes allow controlled experimentation with new approaches. The key is viewing security as an enabler of innovation rather than an obstacle—secure systems build client trust that enables adoption of new services.

What role do fintech partnerships play in banking transformation?

Fintech partnerships allow banks to access innovation and specialized capabilities faster than building in-house. Banks provide regulatory expertise, capital, distribution networks, and brand trust. Fintechs contribute agility, customer-centric design, and technology platforms. This collaborative model accelerates transformation for both parties. The most successful partnerships clearly define roles, align incentives, and integrate systems to create seamless client experiences.

How can traditional banks compete with digital-native competitors?

Traditional banks possess advantages digital natives lack: established client relationships, regulatory expertise, balance sheet strength, and trusted brands. Success requires leveraging these strengths while addressing weaknesses in technology and agility. Banks that modernize core systems, adopt agile operating models, and design client experiences that rival digital competitors can maintain relevance. The institutions that fail are those that ignore the competitive threat or respond too slowly.

What metrics indicate successful digital transformation in corporate banking?

Successful transformation shows up across multiple dimensions: improved client satisfaction scores and Net Promoter Scores, increased digital adoption rates, reduced operational costs and improved efficiency ratios, faster time-to-market for new products, revenue growth from digital channels, and risk metrics like reduced fraud and improved compliance. The specific metrics matter less than establishing clear baselines, tracking progress consistently, and adjusting strategy based on results.