Digital Transformation in Financial Services 2026

Quick Summary: Digital transformation in financial services involves integrating advanced technologies like AI, cloud computing, and mobile banking to modernize operations, enhance customer experiences, and remain competitive. Financial institutions are adopting fast payment systems, mobile platforms, and data analytics to meet evolving consumer expectations while navigating regulatory challenges and security concerns.

The financial services sector stands at a pivotal moment. Traditional banks, credit unions, and insurance companies face mounting pressure to modernize or risk obsolescence. Technology-enabled innovation isn't just changing how transactions happen—it's fundamentally reshaping the relationship between financial institutions and their customers.

According to research from the Federal Reserve, mobile banking adoption has accelerated dramatically over the past decade. Smartphones and internet connectivity have given consumers new tools for managing money, fundamentally altering customer expectations. Financial institutions that fail to meet these digital expectations find themselves losing market share to nimbler competitors.

But here's the thing—digital transformation doesn't mean abandoning what works. It means strategically integrating technology to enhance operations while maintaining the trust and relationships that have always been central to finance.

What Digital Transformation Actually Means for Finance

Digital transformation in banking and financial services refers to integrating digital technologies and strategies to optimize operations and enhance personalized experiences. That's the textbook definition, anyway.

In practice, it looks more complex. Financial institutions are deploying everything from artificial intelligence for fraud detection to cloud-based infrastructure for scalability. They're building mobile apps that let customers deposit checks with their phone cameras and using data analytics to offer personalized financial advice.

The Federal Reserve's research on mobile financial services reveals that consumers now access their bank accounts through multiple channels—branch visits, ATMs, desktop websites, and increasingly, mobile devices. This multi-channel approach demands seamless integration across all touchpoints.

Real talk: transformation isn't just about technology. It requires rethinking organizational culture, employee training, regulatory compliance, and customer service approaches. Banks that treat it as purely an IT project typically struggle.

Key Technologies Driving the Transformation

Several core technologies are reshaping the financial landscape. Understanding these building blocks helps clarify how institutions can compete effectively.

Fast Payment Systems and Mobile Platforms

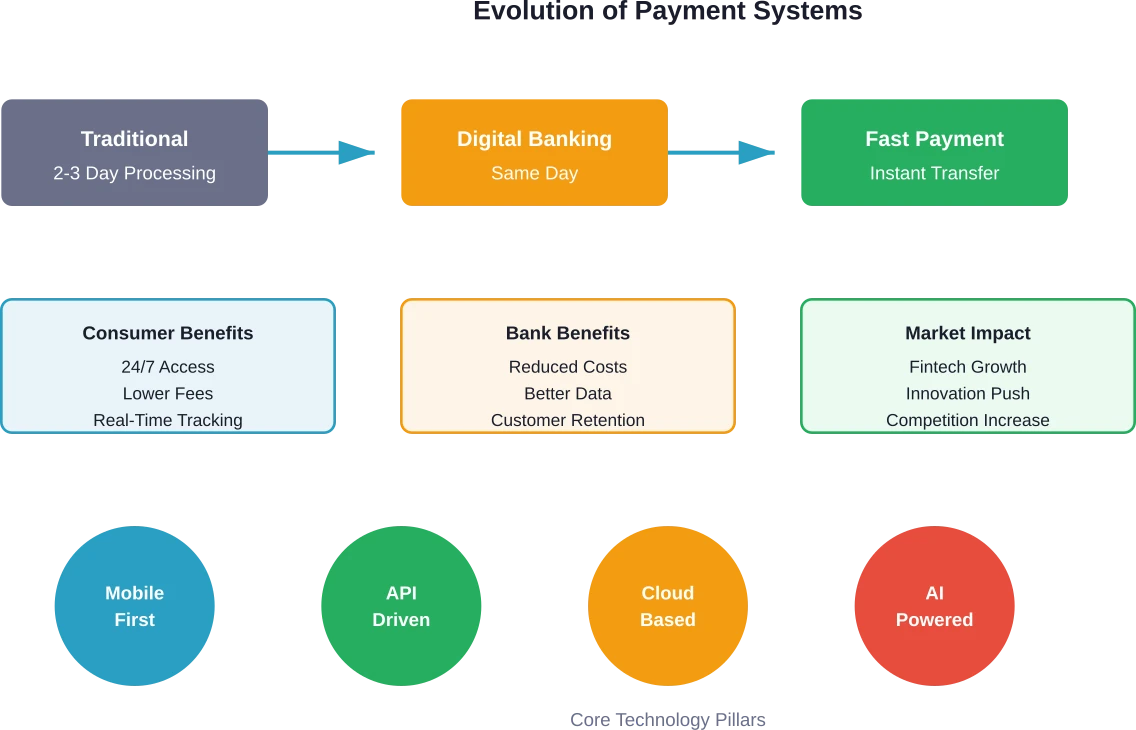

Retail fast payment systems have emerged as major catalysts for digital finance. According to research from the Bank for International Settlements, systems like Brazil's Pix, India's UPI, and Switzerland's TWINT have stimulated widespread adoption of digital finance applications.

These platforms enable instant transfers, often at no cost to consumers. The speed and convenience represent a quantum leap from traditional payment processing that could take days. Fast payment systems also create infrastructure that fintech companies and traditional banks can build upon.

Mobile banking specifically has transformed how consumers interact with financial services. Federal Reserve research indicates that of those with a bank account, 61 percent had used their mobile phone to check account balance or recent transactions. Survey respondents completed the mobile banking survey in approximately 12 minutes (median time), suggesting growing familiarity with these platforms.

Artificial Intelligence and Data Analytics

AI applications in financial services extend far beyond chatbots. Machine learning algorithms detect fraudulent transactions by identifying patterns humans might miss. Predictive analytics help banks assess credit risk more accurately. Natural language processing enables automated customer service that actually understands context.

Data analytics transforms raw information into actionable insights. Banks can identify which products specific customer segments need, predict when someone might be ready for a mortgage, or spot early warning signs of financial distress. This personalization was impossible at scale before modern computing power.

The challenge? Privacy concerns and regulatory compliance. Financial regulators worldwide are grappling with how to oversee these rapidly evolving technologies while protecting consumers.

Cloud Computing and Infrastructure

Cloud-based infrastructure offers scalability that traditional on-premises systems can't match. Banks can spin up new services quickly, handle transaction spikes without expensive hardware investments, and access cutting-edge security tools maintained by major cloud providers.

But wait. Cloud adoption in finance hasn't been straightforward. Regulatory requirements around data sovereignty, concerns about third-party risk, and the complexity of migrating legacy systems have slowed adoption compared to other industries.

Many institutions now pursue hybrid cloud strategies—keeping sensitive core banking systems on-premises while moving customer-facing applications and analytics to the cloud.

![]()

Get Clarity on Your Financial Platform Before You Build

Digital transformation in financial services often involves multiple layers - payments, data processing, integrations, and compliance. The problem is not the idea, it’s figuring out what actually needs to be built and how much it will cost.

OSKI Solutions works with teams at this early stage. They help break down complex financial systems into clear technical requirements, covering integrations, architecture, and functionality before development starts. Their work includes custom software, API integrations, and cloud-based systems built around real business workflows.

With OSKI, you can:

- turn financial processes into structured system requirements

- plan integrations across platforms and services

- understand cost and timeline before committing

If you need a clear plan before building your financial platform - start with OSKI Solutions.

Transform Financial Services with Digital Innovation

Modernize financial operations with secure, scalable digital solutions. From automation and advanced analytics to customer platforms and integrations, we help financial organizations improve efficiency and deliver better services.

The Regulatory Dimension: SupTech and Compliance

Financial regulators face their own digital transformation challenges. How can oversight keep pace with innovation? The answer increasingly lies in supervisory technologies, or SupTech.

Research published in the Harvard Data Science Review explores how financial regulators are deploying technology to supervise the fast-evolving financial services ecosystem. The 2007-2008 financial crisis left lasting concerns about regulatory capability, and novel technological approaches are being deployed at unprecedented rates.

SupTech enables regulators to analyze massive datasets, monitor markets in real-time, and identify systemic risks earlier. For financial institutions, this means compliance itself is becoming more automated—both a challenge and an opportunity.

Regulatory technology (RegTech) helps banks meet compliance requirements more efficiently. Automated reporting, real-time transaction monitoring, and AI-powered risk assessment reduce the human burden of compliance while improving accuracy.

How Small Institutions Can Compete

Digital transformation doesn't have to privilege scale and automation exclusively. Research from the California Management Review highlights how small financial institutions can compete in an open-banking world through relationship-first strategies.

The key insight? Small banks and credit unions can't outspend large institutions on technology. But they can leverage digital tools to enhance what they already do well—personal relationships and community connections.

Relationship-first digital transformation means using technology to deepen customer understanding rather than replace human interaction. A community bank might use data analytics to identify when small business clients need financing, then have relationship managers reach out personally rather than sending automated offers.

Open banking regulations, which require banks to share customer data (with permission) through APIs, create opportunities for smaller players. They can partner with fintech companies to offer services they couldn't build alone—wealth management tools, budgeting apps, or specialized lending platforms.

Major Trends Shaping the Future

Several interconnected trends are accelerating transformation across financial services. Understanding these helps institutions prioritize investments.

Open Banking and API Ecosystems

Open banking regulations in Europe, the UK, and increasingly other markets require banks to share customer data through standardized APIs. This shifts banks from closed systems to platforms that can integrate with third-party services.

For consumers, this means financial management apps that aggregate accounts from multiple banks, easier switching between providers, and access to innovative services built on banking infrastructure. For banks, it represents both competitive threat and opportunity to become embedded in customers' daily financial lives.

Embedded Finance

Financial services are increasingly embedded in non-financial contexts. Buy-now-pay-later options at checkout. Insurance embedded in ride-sharing apps. Banking services integrated into accounting software for small businesses.

This trend blurs traditional industry boundaries. Retailers, technology companies, and service providers partner with banks to offer financial products without customers needing to visit a bank at all. The bank becomes invisible infrastructure.

Blockchain and Digital Assets

Federal Reserve Governor Christopher J. Waller spoke about the next frontier of payments innovation at the 2025 Sibos conference (September 29, 2025). While central bank digital currencies remain debated, blockchain technology shows promise for cross-border payments, securities settlement, and trade finance.

Digital assets—from cryptocurrencies to tokenized securities—represent another frontier. Traditional financial institutions are cautiously exploring how to custody, trade, and integrate these assets while managing risk and regulatory uncertainty.

Cybersecurity and Privacy

As financial services become more digital, security threats multiply. Phishing attacks, ransomware, data breaches, and sophisticated fraud schemes constantly evolve. Cybersecurity isn't a one-time investment but an ongoing arms race.

Privacy regulations like GDPR in Europe and CCPA in California add complexity. Banks must balance using customer data for personalization with respecting privacy rights and meeting regulatory requirements. Transparency about data usage is becoming a competitive differentiator.

Implementation Challenges and Solutions

Knowing what to do is easier than actually doing it. Financial institutions face significant hurdles in executing transformation strategies.

Legacy System Integration

Many banks run critical operations on decades-old mainframe systems. These legacy systems are reliable and time-tested, but they weren't designed for APIs, real-time processing, or integration with modern applications.

Ripping out and replacing core banking systems is risky, expensive, and time-consuming. Most institutions instead pursue gradual modernization—wrapping legacy systems with modern APIs, moving specific functions to new platforms incrementally, and building new capabilities alongside existing infrastructure.

Cultural Transformation

Technology is only part of the equation. Organizational culture often poses the biggest obstacle. Banks have traditionally been risk-averse, hierarchical organizations with slow decision-making processes. Digital transformation requires agility, experimentation, and tolerance for failure.

Employees need training not just on new systems but on new ways of working. Cross-functional teams, agile methodologies, and customer-centric thinking represent fundamental shifts for many financial institutions.

Talent Acquisition and Retention

Financial institutions compete with technology companies for data scientists, software engineers, and digital product managers. But they often can't match tech-company compensation or offer the same work culture.

Some banks address this through acquisitions—buying fintech startups to acquire both technology and talent. Others build innovation labs in tech hubs separate from traditional corporate offices. Partnerships with universities and investment in upskilling existing employees also help close talent gaps.

|

Challenge |

Traditional Approach |

Modern Solution |

Implementation Timeline |

|---|---|---|---|

|

Legacy System Modernization |

Full replacement project |

Incremental API wrapping and microservices |

2-5 years |

|

Customer Experience |

Branch-focused service |

Omnichannel with mobile priority |

1-3 years |

|

Data Management |

Siloed databases by product |

Unified data lake with governance |

2-4 years |

|

Regulatory Compliance |

Manual review and reporting |

Automated RegTech solutions |

1-2 years |

|

Security |

Perimeter defense |

Zero-trust architecture with AI monitoring |

Ongoing |

|

Innovation |

Centralized IT department |

Distributed teams with agile methodology |

1-2 years |

Measuring Success: Key Performance Indicators

How do financial institutions know if transformation efforts are working? Several metrics provide insight.

Customer satisfaction scores and Net Promoter Scores track whether digital initiatives actually improve experiences. Digital adoption rates—the percentage of customers actively using mobile apps or online services—indicate whether investments are reaching target audiences.

Operational efficiency metrics matter too. Cost per transaction typically drops as processes digitize. Time to market for new products and features should decrease as systems become more agile. Employee productivity often increases when manual tasks are automated.

Revenue metrics tell the ultimate story. Digital channels should drive customer acquisition, increase cross-selling success, and improve retention. Institutions that effectively transform typically see digital channels become their primary growth engine.

Looking Ahead: The Next Frontier

Federal Reserve Governor Christopher J. Waller spoke about the next frontier of payments innovation at the 2025 Sibos conference (September 29, 2025). The pace of change shows no signs of slowing.

Quantum computing looms on the horizon, potentially revolutionizing both cryptography and computational finance. Its emergence could require complete rethinking of security approaches while enabling previously impossible calculations.

Generative AI is moving beyond chatbots to content creation, code generation, and complex analysis. Financial advisors might use AI assistants that draft personalized investment strategies. Compliance teams could deploy AI that writes regulatory reports.

The metaverse and spatial computing represent wildly different interface paradigms. Will customers manage finances through virtual reality branches? Handle transactions through augmented reality overlays? These possibilities seemed like science fiction just years ago.

Climate risk and sustainable finance are driving new data requirements and analytical approaches. Financial institutions need to assess environmental risks in loan portfolios, report on sustainability metrics, and offer products aligned with ESG principles.

Practical Steps to Begin Transformation

For institutions wondering where to start, several practical steps provide solid footing.

Begin with customer research. What pain points do customers experience? What do they value most? Where are they already using digital tools? Surveys, interviews, and behavioral data all provide insights that should drive priorities.

Conduct a technology audit. What systems currently exist? Where are integration gaps? What technical debt needs addressing? Understanding the current state prevents unrealistic plans.

Start small with pilot programs. Test new capabilities with limited customer segments before full rollout. This reduces risk while providing learning opportunities. A mobile check deposit feature piloted with a few thousand customers reveals issues before millions of customers encounter problems.

Invest in people alongside technology. Training programs, hiring strategies, and cultural initiatives should run parallel to technical implementations. The best systems fail without capable people operating them.

Establish clear governance. Who decides on technology investments? How are priorities set? What metrics define success? Ambiguity in governance leads to conflicting initiatives and wasted resources.

Build security in from the start. Bolting security onto systems after development creates vulnerabilities. Security architecture, privacy by design, and regular testing should be non-negotiable components of every initiative.

Frequently Asked Questions

What is digital transformation in financial services?

Digital transformation in financial services involves integrating advanced technologies like artificial intelligence, cloud computing, mobile platforms, and data analytics to modernize operations, enhance customer experiences, and create new business models. It's not just about digitizing existing processes but fundamentally rethinking how financial institutions operate and serve customers in a technology-enabled world.

Why is digital transformation important for banks?

Digital transformation is essential for banks to remain competitive as customer expectations evolve, fintech companies disrupt traditional models, and operational efficiency becomes critical. According to the Federal Reserve's research, consumers increasingly expect seamless digital experiences across all channels. Banks that fail to transform risk losing customers to more digitally savvy competitors while facing higher operating costs from outdated systems.

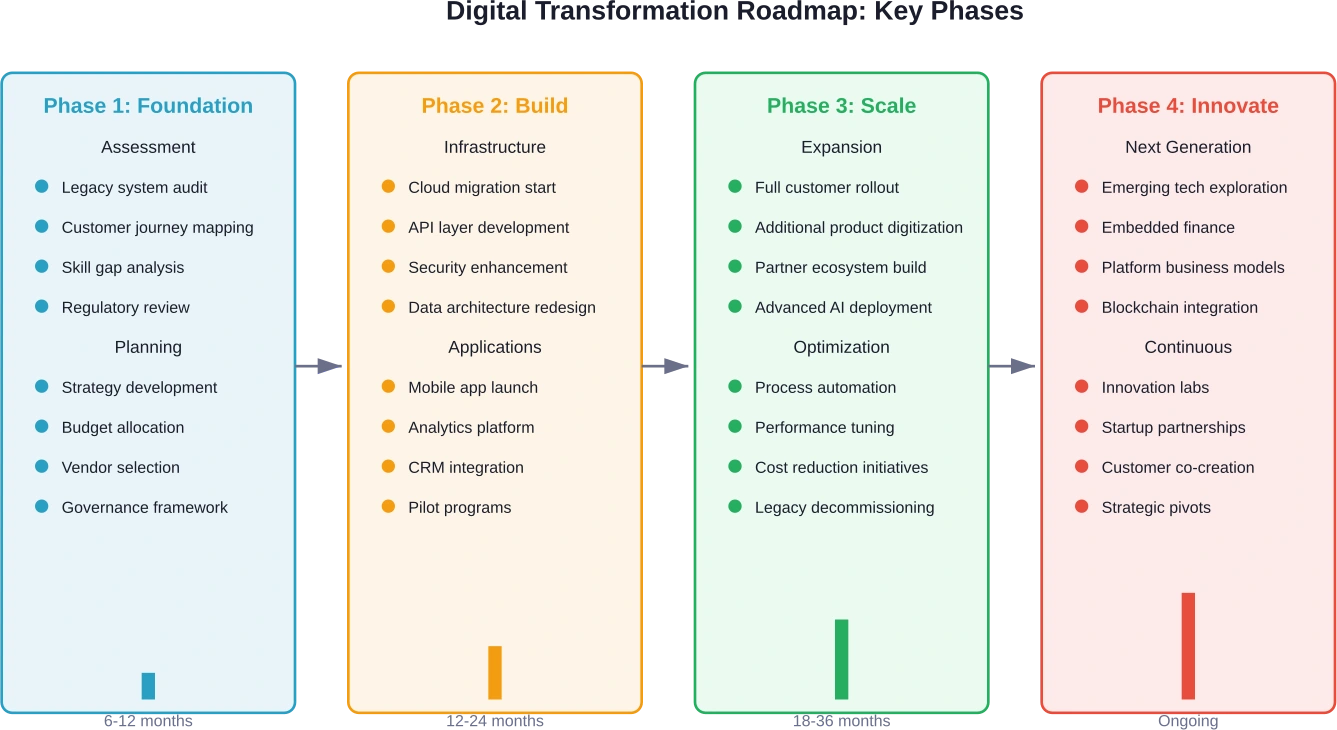

How long does digital transformation take?

Complete digital transformation typically takes 3-5 years for most financial institutions, though it's more accurately viewed as an ongoing journey rather than a destination. Initial foundation phases might take 6-12 months for assessment and planning, followed by 12-24 months for core system builds, and 18-36 months for scaling efforts. However, continuous innovation should become part of organizational culture, meaning transformation never truly "ends."

What are the biggest challenges in financial services digital transformation?

The primary challenges include integrating or replacing legacy systems that are decades old, changing organizational culture from risk-averse to innovation-friendly, navigating complex regulatory requirements, acquiring and retaining technology talent, and managing cybersecurity risks. Many institutions also struggle with data quality and governance issues when attempting to implement advanced analytics.

How can small banks compete with large institutions in digital transformation?

Small financial institutions can compete by focusing on relationship-first digital strategies that leverage technology to enhance personal service rather than replace it. Research from the California Management Review suggests partnering with fintech companies through open banking APIs, focusing on niche markets or communities, and using data analytics to provide personalized service at scale. Small institutions can be more agile in decision-making and implementation than large bureaucratic organizations.

What technologies are most important for financial services transformation?

The most critical technologies include cloud computing for scalable infrastructure, artificial intelligence and machine learning for fraud detection and personalization, mobile platforms that provide primary customer interfaces, fast payment systems for instant transactions, API architectures enabling open banking, data analytics platforms for insights, and robust cybersecurity systems. The specific priority depends on each institution's current state and strategic goals.

How does digital transformation impact financial regulation?

Digital transformation is affecting both how institutions are regulated and how regulators operate. Financial regulators are deploying supervisory technologies to monitor fast-evolving markets and technology deployments more effectively. Institutions benefit from regulatory technology solutions that automate compliance, reporting, and risk management. Research in the Harvard Data Science Review explores how regulators are adapting to oversee technologically enabled financial services while protecting consumers and market stability.

Conclusion: The Imperative to Transform

Digital transformation in financial services isn't optional anymore. The question isn't whether to transform but how quickly and effectively institutions can execute their strategies.

Technology continues advancing at accelerating rates. Customer expectations keep rising. Competitive threats emerge from unexpected quarters. Financial institutions that treat transformation as a discrete project rather than an ongoing strategic priority will find themselves perpetually behind.

But the opportunity is equally significant. Institutions that successfully navigate transformation can operate more efficiently, serve customers better, reach new markets, and create entirely new revenue streams. They can make financial services more accessible, personalized, and valuable.

The most successful transformations balance technological capability with human judgment, efficiency with security, innovation with stability. They recognize that finance ultimately remains about trust, relationships, and helping people and businesses achieve their goals—just with better tools.

Start with clear strategic vision, invest in both technology and people, measure progress rigorously, and remain adaptable as circumstances change. The future of financial services belongs to institutions that embrace transformation while staying true to their fundamental mission.

Ready to begin your digital transformation journey? Assess your current capabilities, identify your biggest opportunities, and take that first concrete step. The future won't wait.