Digital Transformation in Banking: 2026 Guide and Trends

Quick Summary: Digital transformation in banking integrates advanced technologies like cloud computing, AI, and data analytics to modernize operations, enhance customer experiences, and improve security. Banks are adopting mobile platforms, automated systems, and real-time payment solutions to meet evolving consumer expectations while maintaining regulatory compliance. This shift enables financial institutions to operate more efficiently, reduce costs, and compete with emerging fintech challengers.

The banking industry stands at a crossroads. Traditional financial institutions face pressure from multiple directions—tech-savvy customers demanding seamless digital experiences, fintech startups offering innovative solutions, and regulatory bodies pushing for enhanced security measures.

Digital transformation isn't just about adding a mobile app or updating legacy systems. It represents a fundamental shift in how banks operate, interact with customers, and deliver value. Financial institutions that embrace this change position themselves for long-term success. Those that don't risk becoming irrelevant.

According to Federal Reserve Governor Michael S. Barr (October 2025), stablecoins, artificial intelligence, real-time payments, and richer payment metadata offer significant improvements to payments. Banks must adapt or face displacement by more agile competitors.

What Digital Transformation Really Means for Banking

Digital transformation in banking involves integrating digital technologies and strategies to optimize operations and enhance personalized experiences. This goes beyond surface-level changes—it touches every aspect of banking operations.

The technology fundamentally reshapes how banks process transactions, manage data, assess risk, and serve customers. Mobile banking apps, online account management, and digital payment systems represent just the visible layer of a deeper transformation.

Behind the scenes, banks are deploying cloud infrastructure, implementing machine learning algorithms, and building data analytics platforms. These technologies enable faster decision-making, improved fraud detection, and more personalized service offerings.

According to a Federal Reserve FEDS Note from December 2025, the rapid growth of stablecoins could fundamentally reshape the structure and functions of banking and influence the established intermediation role of banks. This technological shift affects everything from deposits to credit to overall banking system architecture.

Why Banks Can't Ignore Digital Transformation

Customer expectations have shifted dramatically. People who shop on Amazon, order from Uber, and stream Netflix expect the same seamless experience from their bank. They want instant access, personalized recommendations, and frictionless transactions.

But here's the thing—consumer demand represents just one driver. Operational efficiency matters too. Legacy systems cost banks millions in maintenance while limiting their ability to innovate. Modern cloud-based platforms reduce these costs while enabling rapid deployment of new features.

Security concerns also push transformation forward. According to TierPoint research, 91% of Americans decide which bank to use based on fraud protection and other security features. This places it as the most important factor, on equal footing with quality customer service and digital banking access.

Competition from fintech companies adds another layer of urgency. These startups operate without the burden of legacy infrastructure, allowing them to move fast and capture market share. Traditional banks must modernize to compete.

According to Federal Reserve Governor Lael Brainard (February 2020), in China, the majority of consumers and businesses participate in two mobile payment networks, Alipay and WeChat Pay, which by some accounts handled more than $37 trillion. This demonstrates how quickly digital platforms can dominate when they achieve scale and network effects.

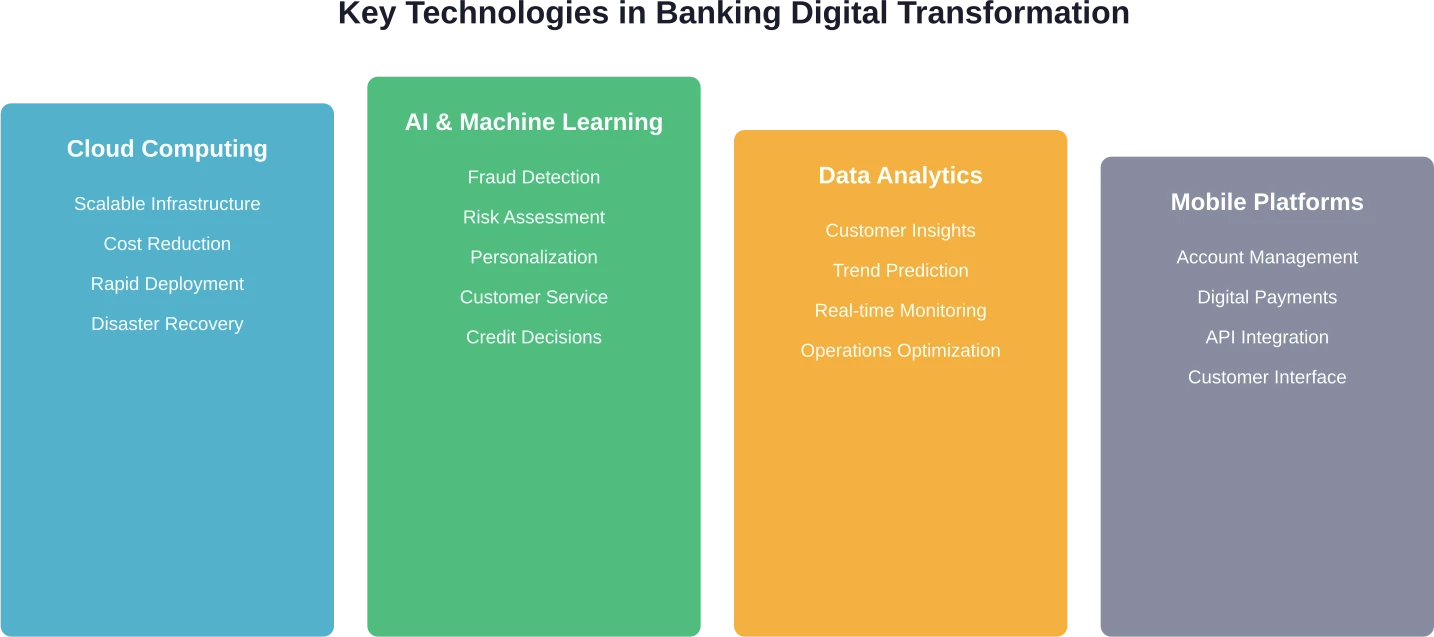

Core Technologies Driving Banking Transformation

Several key technologies form the foundation of digital banking transformation. Each plays a distinct role in modernizing financial services.

Cloud Computing Infrastructure

Cloud platforms provide the scalable infrastructure banks need to handle fluctuating workloads and deploy new services quickly. Instead of maintaining expensive data centers, financial institutions leverage cloud providers for storage, processing, and application hosting.

This shift reduces capital expenditure while increasing flexibility. Banks can scale resources up or down based on demand, paying only for what they use. Cloud also enables faster disaster recovery and improved business continuity.

Artificial Intelligence and Machine Learning

AI powers everything from chatbots handling customer inquiries to sophisticated fraud detection systems analyzing millions of transactions. Machine learning algorithms identify patterns humans might miss, improving risk assessment and credit decisions.

These technologies also enable personalization at scale. Banks can analyze customer behavior and preferences to offer tailored product recommendations, optimized interfaces, and proactive financial advice.

Data Analytics Platforms

Banks generate enormous volumes of data daily. Advanced analytics platforms turn this raw information into actionable insights. Financial institutions use these tools to understand customer needs, predict market trends, and optimize operations.

Real-time analytics enable immediate responses to emerging threats or opportunities. Banks can identify fraudulent transactions as they occur, adjust lending strategies based on current conditions, and personalize customer interactions in the moment.

Mobile and Digital Platforms

Mobile banking apps have become the primary interface between banks and customers. These platforms must deliver comprehensive functionality—account management, payments, deposits, loan applications, and customer support—all within an intuitive interface.

Digital platforms also extend to web applications, API integrations, and partner ecosystems. Banks are building open banking capabilities that allow third-party developers to create innovative services on top of banking infrastructure.

Plan Your Banking Software Before You Build

Digital transformation in banking usually involves complex systems - integrations, security, compliance, and customer-facing apps. The challenge is turning these requirements into a clear technical plan and realistic budget before development starts.

OSKI Solutions works with teams at this early stage. They help define system architecture, integrations, and feature scope so you understand what needs to be built and what it will cost before committing to development. Their work includes custom software, API integrations, cloud systems, and fintech solutions.

With OSKI, you can:

- define core banking and app features

- plan integrations with existing systems

- estimate cost and timeline before development

Get a clear scope and cost for your banking system - talk to OSKI Solutions.

Transform Banking with Digital Innovation

Modernize banking systems with secure and scalable digital solutions. From core system upgrades and automation to AI-driven analytics and customer platforms, we help financial institutions improve efficiency and deliver better services.

Real-World Applications Transforming Banking Operations

Theory matters less than execution. Here's how banks are actually implementing digital transformation across different operational areas.

Mobile Banking and Account Management

Customers now handle most banking tasks through smartphones. Mobile apps enable check deposits, bill payments, fund transfers, and account monitoring—all without visiting a branch. Some banks have achieved over 80% mobile adoption among active customers.

Advanced features include biometric authentication, personalized spending insights, and instant loan pre-approvals. The mobile experience becomes the primary brand touchpoint for many customers.

Automated Lending and Credit Decisions

Traditional loan applications involved extensive paperwork and weeks of waiting. Digital platforms now deliver instant credit decisions using automated underwriting algorithms. These systems analyze credit history, income verification, and risk factors in seconds.

Machine learning models continuously improve by learning from past decisions. This increases approval accuracy while reducing default rates. Small business loans that once took months now complete in days.

Payment Innovation and Real-Time Transfers

Payment innovation is accelerating, with new technologies enabling instant settlement. Real-time payment systems allow immediate transfers between accounts, eliminating the traditional multi-day clearing process.

Digital wallets, contactless payments, and peer-to-peer transfer apps have become standard offerings. Banks must integrate these capabilities to remain competitive with fintech alternatives like Venmo and Cash App.

Enhanced Fraud Prevention

AI-powered fraud detection systems monitor transactions in real-time, identifying suspicious patterns instantly. These systems analyze factors like transaction location, amount, merchant type, and historical behavior to flag potential fraud.

When anomalies appear, systems can automatically block transactions and alert customers via push notification. This proactive approach reduces fraud losses while minimizing false positives that frustrate legitimate customers.

|

Application Area |

Traditional Approach |

Digital Transformation |

Key Benefit |

|---|---|---|---|

|

Account Opening |

Branch visit, paper forms, 5-7 days |

Mobile app, digital verification, 10 minutes |

95% faster onboarding |

|

Loan Processing |

Manual review, weeks of waiting |

Automated underwriting, instant decisions |

Reduced processing time |

|

Fraud Detection |

Rule-based systems, delayed alerts |

AI monitoring, real-time blocking |

Lower fraud losses |

|

Customer Service |

Phone calls, long wait times |

AI chatbots, 24/7 availability |

Instant responses |

|

Payments |

3-5 day clearing, limited hours |

Real-time settlement, always available |

Immediate access to funds |

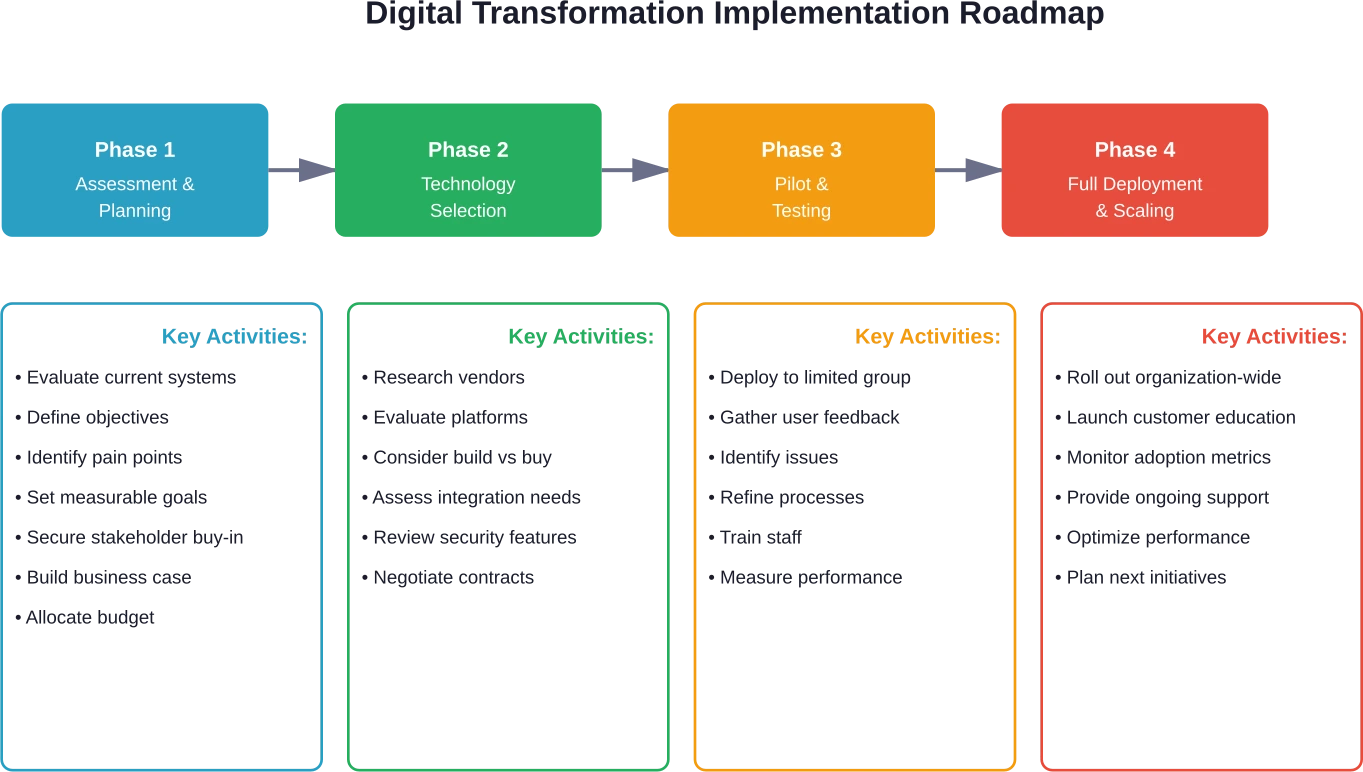

Strategic Implementation Approaches

Successful digital transformation requires more than purchasing new technology. Banks need a comprehensive strategy that addresses people, processes, and systems.

Assess Current State and Define Goals

The first step involves honest evaluation of existing capabilities and clear articulation of transformation objectives. What specific problems need solving? Which customer pain points require attention? Where do operational inefficiencies create the most drag?

Goals should be specific and measurable. Rather than vague aims like "improve customer experience," effective targets specify "reduce account opening time from 7 days to 24 hours" or "achieve 75% mobile banking adoption within 18 months."

Prioritize High-Impact Initiatives

Banks can't transform everything simultaneously. Smart implementation focuses on initiatives offering the highest return relative to effort and risk. Quick wins build momentum and demonstrate value to stakeholders.

A study of Chinese commercial banks (2011-2021) found that digital transformation improved operational capabilities, with non-rural commercial banks and those in growth and maturity stages showing stronger benefits than rural banks or those in recession phases.

Build or Partner for Capabilities

Financial institutions face a fundamental choice: build proprietary systems or partner with technology providers. Large banks often develop custom solutions for competitive differentiation. Smaller institutions typically leverage vendor platforms to accelerate deployment.

According to a 2026 California Management Review article by Kristal et al., many small and mid-sized financial institutions pursue relationship-first digital transformation, using digital tools to amplify trust and relational continuity rather than replace them.

Manage Change and Adoption

Technology deployment represents just half the battle. Employees must learn new systems, processes need updating, and customers require education. Effective change management addresses resistance and ensures smooth transitions.

Training programs, clear communication, and ongoing support help staff adapt. Customer education through tutorials, support resources, and guided onboarding drives adoption of new digital channels.

Navigating Common Transformation Challenges

Digital transformation sounds great in theory. Implementation reveals significant obstacles that can derail initiatives without proper planning.

Legacy System Integration

Most banks operate on decades-old core banking systems. These platforms handle critical functions but weren't designed for modern digital integration. Replacing them entirely carries enormous risk and cost.

The solution often involves building API layers that allow new digital applications to interface with legacy systems without requiring complete replacement. This approach enables gradual modernization while maintaining operational stability.

Regulatory Compliance and Security

According to Item 106 of Regulation S-K, the SEC requires companies to describe the board of directors’ oversight of risks from cybersecurity threats.

Banks face potential regulatory actions if they fail to meet these expectations, and remediation efforts require significant resources. Digital transformation initiatives must incorporate security and compliance from the design phase rather than treating them as afterthoughts.

The regulatory environment continues evolving. The Federal Reserve notes that frameworks like proposed stablecoin regulations raise important questions about their impact on traditional banking, affecting everything from deposits to credit to financial intermediation structure.

Talent and Skills Gaps

Traditional banking expertise doesn't automatically translate to digital capabilities. Banks need data scientists, cloud architects, UX designers, and cybersecurity specialists—roles that didn't exist in banking a decade ago.

Competing with tech companies for this talent proves difficult. Banks must either develop competitive compensation packages, invest heavily in training existing staff, or partner with technology firms that provide specialized expertise.

Cultural Resistance to Change

Established organizations develop ingrained ways of working. Employees comfortable with existing processes often resist new systems that require learning different approaches. This cultural inertia can slow or sabotage transformation efforts.

Leadership commitment matters enormously. When executives actively champion digital initiatives and model adoption of new tools, organizational resistance decreases. Clear communication about why changes matter helps employees understand their role in transformation.

|

Challenge |

Impact |

Solution Approach |

|---|---|---|

|

Legacy Systems |

Integration complexity, high costs |

API middleware, phased migration |

|

Cybersecurity |

Regulatory risk, data breaches |

Security-first design, ongoing monitoring |

|

Compliance |

Implementation delays, added costs |

Early regulator engagement, built-in controls |

|

Talent Shortage |

Slower deployment, capability gaps |

Training programs, strategic partnerships |

|

Cultural Resistance |

Low adoption, initiative failure |

Change management, executive sponsorship |

|

Budget Constraints |

Limited scope, delayed timelines |

Phased approach, focus on ROI |

Measuring Digital Transformation Success

Transformation initiatives require clear metrics to evaluate progress and demonstrate value. Effective measurement tracks both operational and customer-facing outcomes.

Operational Efficiency Metrics

Process automation should reduce processing time and operational costs. Banks track metrics like transaction processing speed, cost per transaction, employee productivity, and system uptime. Improvements in these areas indicate successful operational transformation.

Cloud migration often delivers measurable infrastructure cost reductions. Comparing total cost of ownership between legacy data centers and cloud platforms provides concrete ROI data.

Customer Experience Indicators

Digital channel adoption rates show whether customers embrace new capabilities. Banks monitor mobile app active users, online banking penetration, digital transaction volumes, and branch visit frequency.

Customer satisfaction scores, net promoter scores, and complaint volumes provide qualitative feedback. Improvements suggest digital initiatives enhance rather than frustrate customer experiences.

Revenue and Growth Measures

Digital transformation should ultimately drive business results. New account openings through digital channels, cross-sell ratios, customer lifetime value, and overall revenue growth demonstrate commercial impact.

Time-to-market for new products decreases when banks deploy modern development platforms. This agility creates competitive advantages that translate to market share gains.

The Evolving Landscape: What's Next

Digital transformation represents an ongoing journey rather than a destination. New technologies and changing customer expectations ensure continuous evolution.

Open Banking and API Ecosystems

Open banking regulations require banks to share customer data with authorized third parties through secure APIs. This creates opportunities for partnerships and innovative services built on banking infrastructure.

Banks can become platform providers, enabling external developers to create applications that add value for shared customers. This ecosystem approach expands capabilities beyond what any single institution could build alone.

Embedded Finance

Financial services increasingly embed directly into non-financial platforms. Buy-now-pay-later options at checkout, in-app payment capabilities, and integrated lending represent this trend.

Banks must decide whether to power these embedded experiences or risk disintermediation by fintech providers. Strategic partnerships with retailers, marketplaces, and software platforms offer distribution channels beyond traditional banking.

Stablecoins and Digital Assets

According to a Federal Reserve FEDS Note from December 2025 by Jessie Jiaxu Wang, if stablecoin issuers hold their reserves primarily as bank deposits, this would largely maintain overall banking system size while possibly increasing deposit concentration and shifting from insured retail deposits to uninsured wholesale deposits.

Banks exploring digital asset custody, stablecoin integration, and blockchain-based settlement face both opportunities and uncertainties as regulatory frameworks develop.

Advanced AI Applications

Current AI implementations focus primarily on fraud detection and chatbots. Next-generation applications will handle more complex tasks—automated financial planning, predictive risk management, and intelligent process orchestration.

Generative AI could transform customer interactions, enabling natural conversation interfaces that understand context and intent. Banks must balance innovation with risk management as these powerful tools emerge.

Frequently Asked Questions

What does digital transformation mean in banking?

Digital transformation in banking refers to integrating digital technologies throughout financial operations to improve efficiency, enhance customer experiences, and enable new business models. This includes mobile platforms, cloud infrastructure, AI-powered analytics, and automated processes that modernize how banks operate and serve customers.

Why is digital transformation important for banks?

Banks face multiple pressures driving digital transformation: customer expectations for seamless digital experiences, competition from agile fintech startups, operational inefficiencies from legacy systems, and regulatory requirements for enhanced security. Transformation enables banks to reduce costs, improve service quality, and remain competitive in an evolving marketplace.

What technologies drive banking digital transformation?

Key technologies include cloud computing for scalable infrastructure, artificial intelligence and machine learning for automation and personalization, data analytics platforms for insights, mobile applications for customer engagement, and API integrations for ecosystem connectivity. These technologies work together to create comprehensive digital banking capabilities.

What challenges do banks face during digital transformation?

Common challenges include integrating new systems with legacy infrastructure, meeting stringent regulatory and cybersecurity requirements, addressing talent and skills gaps, overcoming cultural resistance to change, and managing transformation costs within budget constraints. Successful banks address these challenges through phased implementation, strong change management, and strategic partnerships.

How long does banking digital transformation take?

Transformation timelines vary based on scope and starting point. Specific initiatives like mobile app deployment might complete in 6-12 months, while comprehensive transformation spanning all operations typically requires 3-5 years. Most banks adopt phased approaches that deliver incremental value rather than attempting wholesale change simultaneously.

How do banks measure digital transformation success?

Success metrics include operational efficiency indicators like reduced processing time and lower costs, customer experience measures such as digital adoption rates and satisfaction scores, and business outcomes including revenue growth and market share gains. Effective measurement combines quantitative metrics with qualitative customer feedback.

Can small banks compete in digital transformation?

Research shows digital transformation doesn't require massive scale to succeed. Smaller financial institutions can compete by focusing on relationship-first approaches that combine personalized service with targeted digital capabilities. Strategic partnerships with technology vendors provide access to advanced platforms without requiring large internal development teams.

Moving Forward with Digital Banking

Digital transformation represents a fundamental shift in banking operations, customer engagement, and competitive positioning. Financial institutions that embrace this change position themselves for long-term relevance and success.

The journey requires strategic planning, significant investment, and organizational commitment. But the cost of inaction exceeds transformation challenges. Banks that fail to modernize face displacement by more agile competitors and diminishing relevance to digitally-native customers.

Successful transformation balances innovation with risk management, ambition with pragmatism, and technology deployment with human-centered design. It's not about technology for technology's sake—it's about using digital capabilities to serve customers better, operate more efficiently, and build sustainable competitive advantages.

The banking industry continues evolving rapidly. New technologies emerge, regulations shift, and customer expectations rise. Digital transformation isn't a one-time project but an ongoing capability that enables continuous adaptation and improvement.

Start where it makes sense for your institution. Identify high-impact opportunities, build a realistic roadmap, secure stakeholder commitment, and begin. Every digital journey starts with that first step—and waiting only makes the gap harder to close.